Looking in the financial rearview mirror, we see that since the 1990s and early 2000’s interest rates have been on a prolonged downward trend. This was amplified during the financial crisis that occurred in 2008 when rates went to historic lows. Until recently, we saw these low rates maintained. Inflation that began to occur after the COVID-19 pandemic resulted in the Bank of Canada ending the run of historically low rates when they began increasing interest rates to levels we haven’t seen in Canada in decades. The plan was that these increases were in place to combat increased inflation. They have also had a significant impact on the mortgage landscape. Let’s look at how interest rates work with mortgages, what someone needs to do to qualify for a mortgage and compare fixed rate versus variable rate mortgages.

In This Article:

Mortgage Interest Rates

There are two ways that interest rates are charged on mortgages, and how each product has its rate set differs a bit. Variable-rate mortgages are tied closely to the prime lending rates that financial institutions charge. Fixed-rate mortgages are more directly linked to the yield that government bonds are generating. This can lead to the creation of confusion. What does the prime lending rate have to do with mortgage rates? How does the Bank of Canada influence things?

- The Bank of Canada plays a central role in the financial sector when it sets its interest rates. The Bank of Canada isn’t a traditional bank that is accessible to consumers in Canada. Instead, it functions as the central bank for the financial services sector. They loan out money to financial institutions and take deposits from them as well. They set something called the ‘overnight rate,’ which outlines what they will charge institutions to access funds for short-term liquidity needs as well as what they would pay them on short-term deposits. Since an increase in the overnight rates increases the costs to the financial institutions accessing the cash they need, when the overnight rate increases, you see lenders change their prime rates to reflect the differences in what it will cost them to access cash.

- The prime lending rate is the amount of interest that major lenders will charge for variable loans and lines of credit. This includes variable-rate mortgages. This rate is tied very closely to the Bank of Canada’s overnight rates because when a bank lends you money, they want to make sure that they are covering their own cost of borrowing from the central bank (and maybe making some profit on the loan as well)

Fixed-rate mortgages are more closely linked to bond yields than they are to the prime rate. This does not mean that changes to the overnight and prime rates don’t affect fixed-rate mortgages, though. If rates are going up, government bonds cost more to acquire, and you will see the fixed-rate mortgage interest amount go up as well. Since government bonds are virtually guaranteed to repay at least their principal amounts at maturity, banks use the yields of these products as the guideline for what a fixed-term mortgage interest rate should be. In a nutshell, as the Bank of Canada decides to move interest rates up and down, you will see corresponding moves in mortgage interest rates.

Qualifying for a Mortgage

In 2016 the mortgage stress test was introduced. This was in response to the concern that, given a prolonged period of low-interest rates, Canadians were entering into more debt than they could handle when interest rates increased. The stress test meant that you needed to qualify for your mortgage based on paying either a rate of 5.25% or whatever your mortgage rate was contractually plus 2%. The idea behind the Stress test is that it created a way of making sure that you could afford your mortgage at renewals in the future, assuming that historically low rates weren’t maintained forever. When rates were low, what you saw was that even if your mortgage interest rate was 2.5%, you would need to be able to qualify as if the rate you were paying was 5.25%. This means that your debt servicing ratios and credit score need to reflect your ability to qualify at a higher rate, even if you aren’t paying it today. When the test was introduced, many people were using the 5.25% rate to qualify; since rates have increased, it is more common for the plus 2% on your contract rate to be applied.

Here’s one major thing to consider. If one of either the fixed or variable rate mortgage has a lower interest rate than the other, and you are maxed out on qualifying, sometimes you don’t get to choose what product you want. You take the one that you qualify for. For example, if you can pass the stress test for a variable rate mortgage but not the fixed rate one, you are going to end up in the variable rate product. The choice is made for you by the qualifying rate. Of course, you can look at changing that in the future, but it is important to weigh both the pros and cons before deciding.

Fixed versus Variable Rate Mortgages

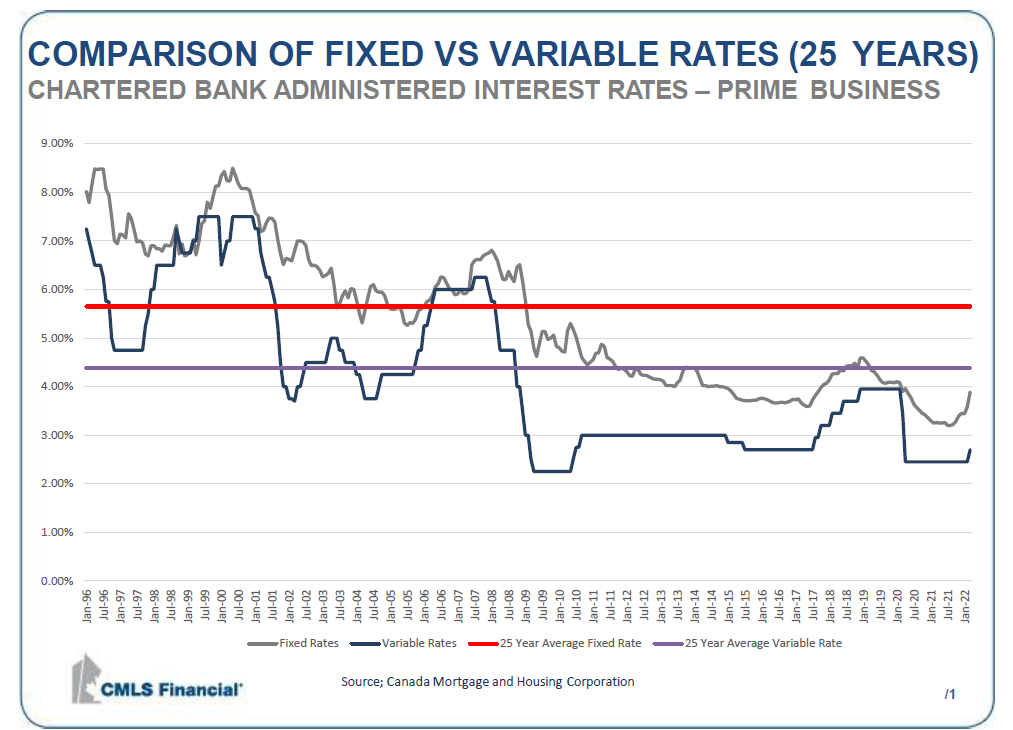

This is a long-term debate. What is the best route for people to take when selecting their mortgage? Fixed or variable? Often the answer comes down to a personal choice. The stability of the fixed mortgage is something that makes some people comfortable. What does this security cost, though? As you can see from the graph below, for the 25 years leading up to January of 2022, if you had used a variable rate mortgage, you wound up ahead of someone who chose the fixed rate option.

What you can also see is that during that 25-year period, there were only a few short windows where the interest rate for the variable rate exceeded the fixed rate. If this is the case, why then do people choose fixed-rate mortgages ever? As I mentioned previously, it often comes down to the security of knowing what your payment will be. People have a difficult time managing their cash flow. The idea that a change in the prime interest rate could lead to an increase in the amount that they need to pay for their mortgage next month is too much for some people to handle. Many homeowners like being able to budget for exactly what their mortgage payment is going to be for the length of their term. You need to have the ability to manage your personal cash flow and the stomach for potential increases in your mortgage payment to make variable rate work for you, even when the data shows that the variable rate product is better over the long run.

Conclusion: Fixed versus Variable Rate Mortgages

We have seen wide variations in interest costs before. In October of 1981, a five-year fixed-rate mortgage had an interest rate of 21.75%; in August of 1981, we saw the highest variable rate mortgages on record when the prime lending rates reached record highs of 22.75%. I had a colleague who started working in the mortgage industry in the 1980s. He talked about arriving at work on Monday mornings and finding envelopes with house keys in them shoved under their door with notes that said that the owners couldn’t make their payments any longer. Contrast this with the recent times when, in the fall of 2021, you could find fixed-rate mortgages for as low as 1.44% for five years. Variable rate plans were seeing rates as low as 0.88% in 2021. Given that we have recently entered a period where interest rates have increased rapidly, we have seen people start to make choices about their mortgages that are based on emotional responses rather than analyzing what the current market dictates. Taking the time to work with a mortgage broker who gets to know you and your situation will help you take emotion out of the calculation and make the right choice that fits you and your plan for the future. If you would like help choosing the product that is best for you, please reach out to us today!