On July 24th the Bank of Canada announced its second consecutive decrease in their prime lending rate. It has been met by the public with happiness after seeing so many increases over recent years. Two consecutive decreases is welcome news. Homeowners in particular are excited to see interest rates decreasing after seeing such a rapid increase in rates over recent years. What exactly does a rate cut mean to you as a consumer though? Let’s take a second and examine how it will affect your expenses.

What is the Bank of Canada Benchmark Rate?

This is perhaps the most important thing to understand. The benchmark interest rate that the Bank of Canada sets is related to how much it costs your bank to borrow money. This means that if the rate goes down then the bank’s borrowing costs also go down, and in turn they can reduce their lending rates and pass that along to the consumer. The key word in that statement is that they can pass it along to the consumer. It doesn’t mean that they have to. In most cases a rate reduction will result in your bank reducing its prime interest rate, but what you may notice is that the speed at which prime is lowered is often a lot slower than when rates are going up. The bottom line is that the Bank of Canada rate announcements actually have nothing to do with you as the end user. As a consumer what matters to you is what your bank is charging as it’s prime interest rate, and that change will take time after any announcement that the Bank of Canada makes to filter through to you.

How will a Change to Prime Lending Rates Affect Me?

This really depends on what type of product you are talking about. The prime lending rate will affect two banking products with an almost immediate effect:

- Variable Rate Mortgages – These mortgages are linked directly to the prime lending rate that your financial institution charges, so any decrease in that rate will result in an immediate decrease in the amount of interest that you pay.

- Lines of Credit – Again, the amount of interest that you pay here is typically tied to the prime lending rate. When prime comes down your interest charges on your line of credit will decrease right away as well.

The major thing that concerns most Canadians as it relates to interest rates is how much they are paying for their mortgage. The reality here is that if you have a fixed rate mortgage there is no immediate effect on you. Your payment won’t change until you reach the end of the fixed term that you signed up for.

How does a Bank of Canada rate Decrease Effect Fixed Rate Mortgage interest rates?

This side of things is a bit more complicated. There is less of a direct effect on fixed rate mortgages from the Bank of Canada interest rate than you might like to see as a homeowner if your mortgage is approaching a renewal point. The reality is that for fixed rate mortgages the yield paid by five year government bonds is more important than the Bank of Canada’s overnight lending rate. The reason for this is that banks often buy five year government bonds as a source of income for themselves. Bonds are low maintenance and banks like to use them as a source of interest income that is easy to manage. They then use the yield from these bonds as a baseline for their five year fixed interest mortgage rates.

At their core bonds do seem like simple investments. You give someone $1000 to buy a bond, they agree to pay you a set amount of interest every year and at the bond’s maturity you get your $1000 back. Where bonds become more complicated is when you look at the secondary markets and how they are bought and sold after purchase but prior to maturity. For a really simple example consider this:

- You purchase a five year bond for $1000 with an interest rate of 5%.

If interest rates go down I can sell my bond on the secondary market for more than the $1000 I paid for it. If I sell it for $1100 the yield of the bond lowers to 4.55%. It still pays $50 in interest but the new owner paid $1100 so $50/$1100 = %4.55

If Interest rates go up and I need to sell my bond on the secondary market I will need to discount the original price to sell it. If I sell it for $900 the yield goes up to %5.55.

How does Bond Yield Affect my Fixed Rate Mortgage?

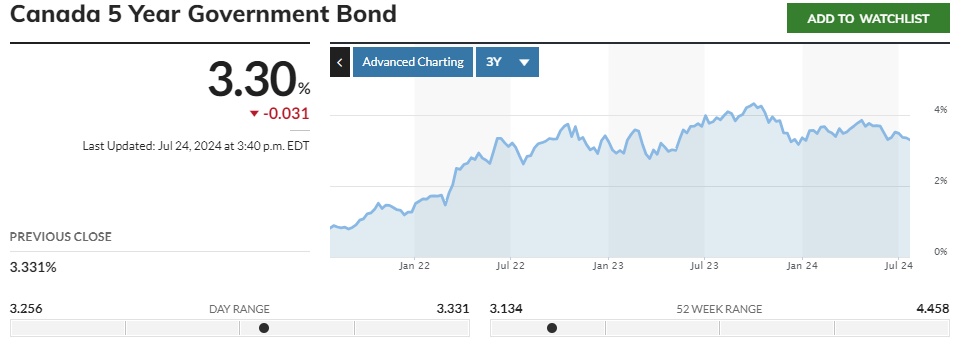

Bond yield is important because the interest rate for fixed rate mortgages is typically set based on a spread over the 5 year bond yield at that time. Consider this chart that shows that in August of 2021 the 5 year bond yield was 0.885% where as of July 24th 2024 it was %3.30

Since how much interest you pay on a fixed rate mortgage is determined via a spread of typically %1-2 over the five year bond yield you can see how the changing interest rates since the battle against inflation started has significantly increased mortgage rates. You also need to know that bond traders are like stock brokers in that when they think that a change in rates is coming they will begin to bid yields up or down on the secondary market, so when a rate cut is expected, bond traders bid down bond yields in anticipation of that reduction in interest rates.

All this means that in the grand scheme of things, fixed interest rates are indirectly influenced by rate changes because when bond traders bid yields lower you tend to see a corresponding decrease in fixed interest mortgage rates.

So is a Bank of Canada Rate Reduction Good News?

If you are someone who uses credit based products a rate reduction is generally good news. With variable rate products where you see that your interest rate is prime rate plus a few points you will see an immediate decrease in the amount of interest you are paying as soon as your bank reduces its prime rate. Remember though, the interest that you pay is determined by the prime rate at the institution that lent you the money, not the Bank of Canada. So just because they announced a rate reduction today you may not see the effects in your accounts for a while.

If you are a homeowner and you are considering how to handle your fixed rate mortgage as rates trend downwards you should reach out to a mortgage broker like the experts at Strata Mortgages. Many economists are predicting that we will continue to see downward movement for interest rates over the next few years. Probably not down to the historic lows seen during the peak of the COVID-19 pandemic, but still lower than they are currently. What does this mean to you? Working with the team at Strata Mortgages will help you build a strategy that will help navigate what to do as rates continue downward. By building a proper plan you can determine what term is right for you (you don’t have to take a five-year fixed rate mortgage, shorter terms are available) to make sure that you feel comfortable with the payment you are going to make and the ability to still capitalize on decreasing rates.

Overall the answer is yes, the rate reduction is good news. It means that the Bank of Canada feels like inflation is more under control and this is good for everyone’s pocketbook. It is also good news for homeowners because they will see their mortgage interest be more manageable.