For years, reverse mortgages in Canada have had a bad reputation.

They were often viewed as a last resort. Something people considered only when they had no other options. At Strata Mortgages Inc., we believe that reputation is increasingly outdated.

The retirement landscape has changed. Home values across Ontario, especially in areas like Muskoka, have grown substantially compared to previous generations. At the same time, retirees are facing higher living costs, longer life expectancies, greater retirement income needs, and the emotional challenge of deciding whether to sell a home they love.

That is why reverse mortgages deserve a more serious conversation.

Today’s reverse mortgage products can allow homeowners to access part of their home equity as tax-free funds, with no required monthly mortgage payments, while maintaining ownership of the home. The Equitable Bank illustration notes that funds may be accessed all at once, as an undrawn reserve for later use, through automatic recurring advances, or through a combination of these options. To see how these numbers align with your goals, explore your options using the Equitable Reverse Mortgage Calculator.

And that flexibility is exactly the point.

“Reverse mortgages used to be something I looked at cautiously. More recently, I’ve started using them as part of our financial planning process, especially with higher-net-worth clients. When structured properly, they can help preserve lifestyle, reduce taxable income pressure, and allow people to stay in the home they love.”

— Tyler Burtch, Founder of Strata Wealth.

In This Article:

- Your Home Is Not Just an Asset

- Case Study: A Muskoka Couple Who Wants to Stay Home

- The RRIF Comparison

- 10-Year Reverse Mortgage Projection

- What If They Sold Today Instead?

- Staying Put Compared With Selling

- Why This Can Make Sense for Higher Net Worth Clients

- Important Considerations

- Final Thought

Your Home Is Not Just an Asset

A home is never just a number on a balance sheet.

For many retirees, it is the place where they raised their children, hosted family dinners, welcomed grandchildren, and built relationships with neighbours who became friends. It is the street they know, the view they love, and the place where life feels familiar.

Selling may create liquidity, but it can also create disruption.

The common retirement idea is simple: Sell the house tax-free, downsize, invest the difference, and use the money for lifestyle. That can work in the right situation, but the math is not always as clean as it first appears.

Selling a home can involve real estate commissions, HST on commissions, legal fees, land transfer tax, moving costs, furniture, renovations, condo fees, and future tax on investment income. Ontario’s HST rate is currently 13%, which matters significantly when calculating the tax on real estate commissions.

That does not mean selling is wrong. It means it should be compared properly.

Case Study: A Muskoka Couple Who Wants to Stay Home

Let’s look at a couple in Muskoka, Ontario. They are 71 and 76 and have lived in their family home for 40 years. Their adult children and grandchildren love the property, and the couple wants to stay there as long as their health allows.

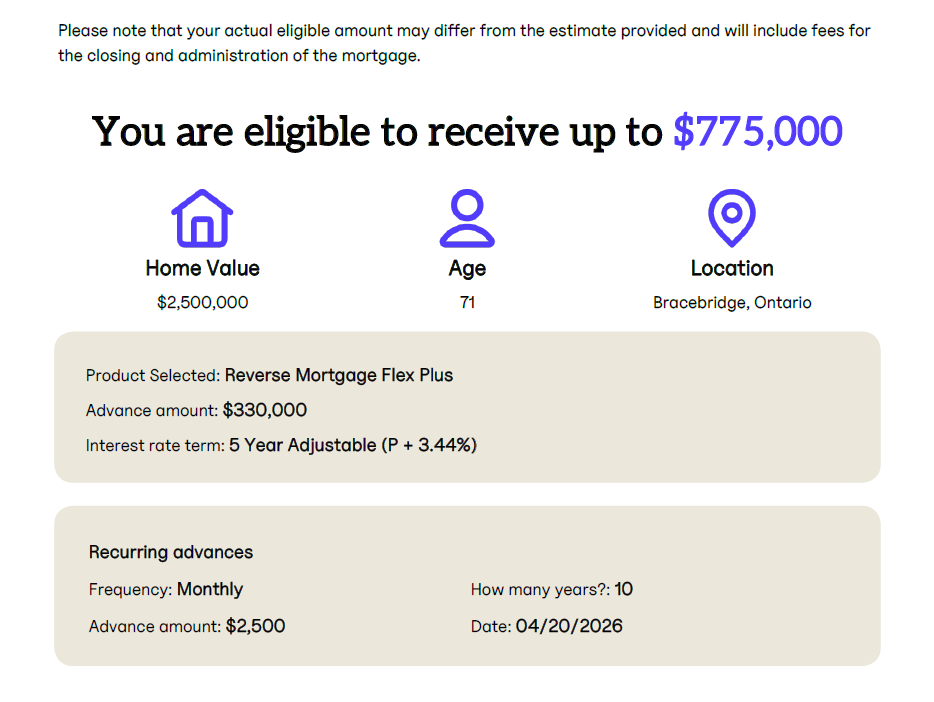

Based on the attached Equitable Bank illustration, their home in Bracebridge, Ontario, is valued at $2,500,000. The youngest spouse is 71. The report shows eligibility of up to $775,000 and models a Reverse Mortgage Flex Plus strategy with an initial advance of $330,000 and recurring monthly advances of $2,500 for 10 years.

There is one important detail: The couple currently has a $330,000 Home Equity Line of Credit (HELOC).

That is why the strategy uses a $330,000 lump sum upfront; it pays off the HELOC, eliminating the need for monthly interest-only payments.

This graphic was taken from the Equitable Life Reverse Mortgage Caculator

Monthly Cash Flow Improvement

At today’s assumed HELOC rate of 5%, the interest-only payment on $330,000 equals $1,375 per month. The reverse mortgage strategy improves monthly cash flow in two ways:

| Source of Improvement | Monthly Amount |

| Recurring reverse mortgage advance | $2,500 |

| Eliminated HELOC interest payment | $1,375 |

| Total Monthly Cash Flow Improvement | $3,875 |

That creates a meaningful retirement cash flow of $46,500 per year; importantly, it is not created by selling the family home.

The RRIF Comparison

To receive the same $46,500 annually from a Registered Retirement Income Fund (RRIF), the couple may need to withdraw significantly more in gross terms.

The CRA states that for Canadian residents outside Quebec, withdrawals over $15,000 are subject to a 30% withholding tax.

| RRIF Withdrawal Breakdown | Amount |

| Net amount needed | $46,500 |

| Withholding tax rate | 30% |

| Estimated gross RRIF withdrawal | $66,428 |

| Estimated tax withheld | $19,928 |

| Estimated net amount received | $46,500 |

Over 10 years, that equates to approximately $664,280 in gross RRIF withdrawals. By using home equity instead, the couple may reduce pressure on registered assets and preserve more flexibility in their retirement income plan.

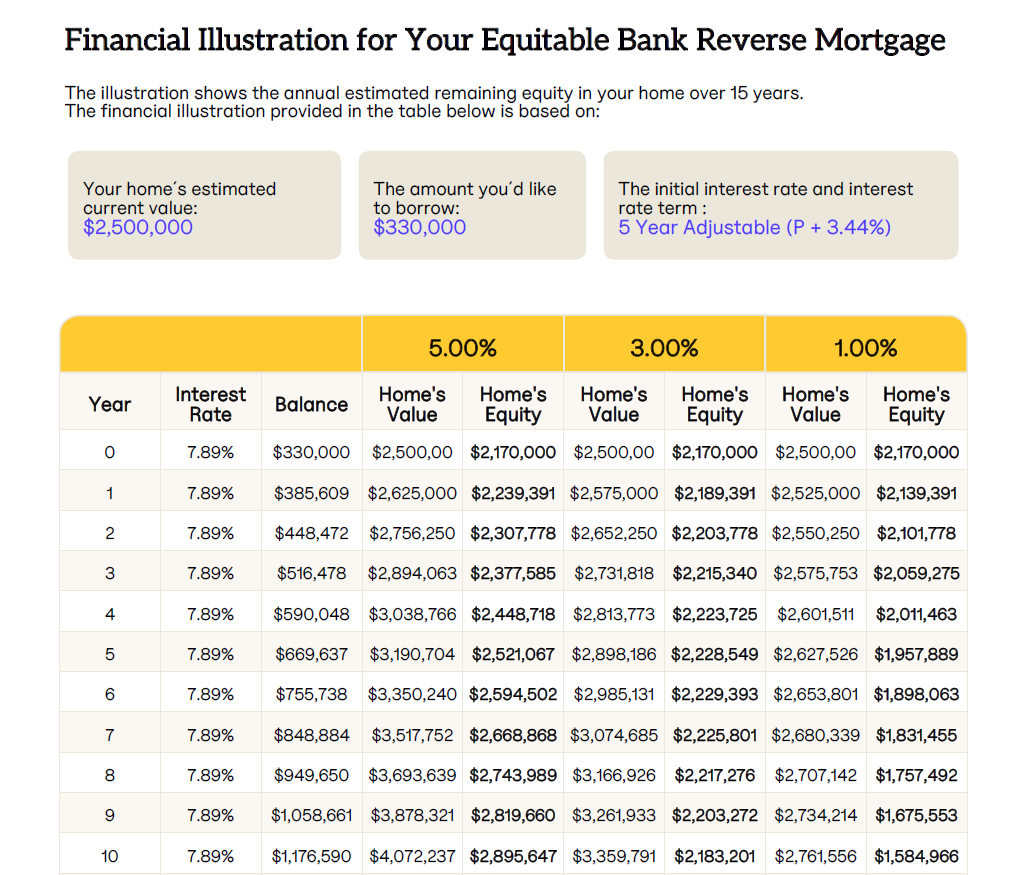

10-Year Reverse Mortgage Projection

The attached Equitable Bank illustration shows the reverse mortgage balance and remaining equity after 10 years. In the best-illustrated scenario, using 5% annual home appreciation, the home is projected to be worth $4,072,237 after 10 years. The reverse mortgage balance is projected at $1,176,590, leaving an estimated remaining equity of $2,895,647.

That is the part people often miss.

Even after paying off the HELOC, receiving $2,500 per month for 10 years, and accruing reverse-mortgage interest, the couple could still have nearly $2.9 million in projected home equity in the best-illustrated scenario.

That is not exactly the financial horror story reverse mortgages are sometimes made out to be.

This graphic was taken from the Equitable Life Reverse Mortgage Caculator

What If They Sold Today Instead?

Now compare that with selling today. Assume they sell the home now for $2,500,000. The existing HELOC would still need to be paid off.

| Immediate Sale Breakdown | Amount |

| Sale price | $2,500,000 |

| HELOC repayment | -$330,000 |

| Real estate commission (5%) | -$125,000 |

| HST on commission (13%) | -$16,250 |

| Estimated moving & transition costs | -$20,000 |

| Estimated amount remaining | $2,008,750 |

This simplified estimate does not include buying another home, land transfer tax, paying rent, condo fees, renovations, new furniture, or tax on investment income generated from the sale proceeds.

If the couple then wanted to replicate the same $46,500 per year of cash flow for 10 years ($465,000 total), that would leave $1,543,750 from the sale proceeds. While this ignores investment returns, future housing costs, and taxes, it clearly shows why selling the house is not always the obvious winner.

Staying Put Compared With Selling

If they stay in the home and use the reverse mortgage strategy, the best-illustrated scenario projects $2,895,647 of remaining home equity after 10 years. If they eventually sold at that 10-year mark, the estimated costs could look like this:

| Year 10 Sale Breakdown | Amount |

| Estimated remaining equity | $2,895,647 |

| Real estate commission (5% of $4,072,237) | -$203,612 |

| HST on commission (13%) | -$26,470 |

| Estimated moving & transition costs | -$20,000 |

| Estimated net value after 10 years | $2,645,565 |

The Comparison:

- Selling Today: Leaves an estimated $1,543,750 (after matching 10 years of cash flow).

- Staying 10 Years: Leaves an estimated $2,645,565 (using the reverse mortgage strategy).

The estimated difference in favour of staying is $1,101,815.

And the couple also gets something the spreadsheet does not fully capture: 10 more years in the home they love.

This graphic was taken from the Equitable Life Reverse Mortgage Caculator

Why This Can Make Sense for Higher Net Worth Clients

A reverse mortgage is not only for people who have no investments.

In many cases, the best use is strategic. It can help higher-net-worth retirees avoid drawing down registered assets too quickly, reduce pressure on taxable income, preserve investment flexibility, and maintain control over when and how they access capital.

This is especially relevant when a client has significant home equity, an existing HELOC, large taxable RRIF withdrawals, rising lifestyle costs, and a strong desire to remain in the family home.

The goal is not to spend the house. The goal is to use a portion of home equity intelligently.

Reverse Mortgages: Important Considerations

Reverse mortgages are not perfect for everyone. Proper planning is critical, and there are key obligations to keep in mind:

- Homeowners must keep property taxes and home insurance paid and current.

- The property must be adequately maintained over time.

- All mortgage obligations must be kept current.

- The actual remaining equity in the home will depend on changes in the home’s value and interest rates.

- Final equity is also impacted by the amount borrowed, prepayments, and any applicable fees or charges.

The old blanket statement that reverse mortgages are universally bad is too simplistic. Used properly, they can be tax-efficient, flexible, and surprisingly powerful.

Reverse Mortgages: Final Thought

Retirement planning is no longer just about investments.

It is about sequencing income, reducing tax pressure, preserving lifestyle, and making sure clients do not feel forced to sell a home before they are ready. For some Canadian retirees, especially those in high-value homes, a reverse mortgage can provide the breathing room they need.

It can pay off costly debt. It can create a monthly cash flow. It can reduce RRIF pressure. It can help preserve the family home. And in the right scenario, it may even leave the estate better positioned than selling too soon.

At the same time, your home retains its full exposure to market appreciation. One key advantage of real estate is that its value increases regardless of how it is financed: mortgage-free, with a traditional mortgage, supported by a HELOC, or structured with a reverse mortgage. That means you’re not sacrificing growth on either side of your balance sheet.

In simple terms, a reverse mortgage helps you keep both assets working for you: your investments continue to grow, and your home can continue to appreciate.

At Strata Mortgages Inc., we believe reverse mortgages deserve a more modern conversation.

Because sometimes the smartest financial move is not cashing out. Sometimes, it is staying put with a better plan.

***Disclaimers

The results in the Equitable Bank Reverse Mortgage Report are based on the information you provided in the Equitable Bank Reverse Mortgage Eligibility Calculator and are estimates and for information purposes only.

Equitable Bank uses reasonable efforts to include accurate and up-to-date information in the calculator, but no warranty is made as to the accuracy or applicability in any case.

The results shows the estimated remaining equity in your home over a period of time. The estimated remaining equity in your home is the difference between the value of the home and the total amount owing on the reverse mortgage at the end of the selected time period. The estimated remaining equity is based on the following assumptions:

• an annual incremental increase in your home value of 3%

• no change in the Equitable Bank Reverse Mortgage Prime Rate

• no principal or interest prepayments are made

This illustration on page 4 assumes: fixed or variable interest rate based on your selected interest rate term; that no principal or interest prepayments are made; and that the balance is made up of only principal and interest.

The actual remaining equity in your home at the end of the selected period of time will depend on several factors, including the change in the value of the home, changes in interest rates, the amount borrowed, the amount of any prepayments and applicable fees or charges.